The Fed raised interest rates by 0.25% on Wednesday to a range of 4.75-5.00%. The upper range of that bound is now 20 times what it was a mere 12 months ago. Rapidly rising rates were always going to put pressure on various sectors of the economy that have benefited from cheap money for the last decade plus (that’s kind of the point). We’ve seen it with startups who scored cheap equity financing a couple years ago that are now having trouble raising up rounds. We’ve seen it with families no longer being able to afford mortgages that are as large (with monthly interest payments almost tripling), resulting in a housing market slowdown. We’ve seen it with the regional bank runs that declines in the values of banks’ bond portfolios have sparked.

The question is now which sector is going to be the domino that tips the economy over the edge into a recession? Commercial real estate seems to have arisen as the most likely candidate, with falling tenancy rates combining with a lot of maturing loans that are coming up for refinancing at today’s much higher rates appearing as storm clouds on the horizon.

We had our third prolonged power outage this year. Again on a Tuesday. An extra-tropical cyclone parked itself just off the coast of San Francisco causing more fallen trees and localized flooding. Power was out for us for about 30 hours, and we ended up spending yet another night in our hotel. We now also have a great view into our neighbor’s back yard because most of our fence is gone. And next Tuesday the forecast is for another period of “excessive rainfall with localized flooding”. Sigh.

Last week, I wrote about the fallout from a protest incident at Stanford Law School. This week, SLS Dean Martinez penned a detailed explanation of why she did what she did. It’s a well written missive, and I agree with almost all of it. However, I had two observations. The first is the practical impact of deciding not to sanction anyone for their behavior, ostensibly because it was too hard to figure out who was breaking policy and who was not. Everyone is instead going to have to sit through a mandatory training. Will this mean that a future protest tactic is to flood a talk with bodies because it’s just too hard to identify who was doing what? The second is that the letter only mentions in passing something about respectful discourse. The letter also expressly notes that asking vulgar and provocative questions when you’re given the microphone is ok and not disruptive. That may be true from the point of view of free speech, but as lawyers, respectful argument is part of the job and—normally—a positive value to encourage. (Try spewing profanities at a judge in court and see how far that gets you.) One protester allegedly called for the judge’s daughters to be raped.

“Our world needs climate action on all fronts—everything, everywhere, all at once,” said UN Secretary-General António Guterres in a speech on Monday. He was referencing an IPCC report which once again is warning we’re nearing the point at which it will not be possible to avoid a rise in the global average temperature by the end of the century of a magnitude that will cause severe human misery. “Unless nations adopt new environmental policies — and follow through on the ones already in place — global average temperatures could warm by 3.2 degrees Celsius (5.8 degrees Fahrenheit) by the end of the century, the synthesis report says. In that scenario, a child born today would live to see several feet of sea level rise, the extinction of hundreds of species and the migration of millions of people from places where they can no longer survive.” It’s going to be a slow burn, but wild weather is going to be increasingly common, and difficult to adapt to in our lifetimes, regardless of where you live in the world.

For those who have the fortune of being able to decide where they want to live and work in the world, I think climate factors are going to rise to one of the top considerations within the next couple of decades. Not just whether the weather is “nice”, but whether that cliffside house or oceanfront view is such a good idea, or whether 100 year flood zones really are 10 year flood zones, or whether water scarcity might be a real problem.

Deal Alert: We use Doordash a lot. If you live near a Lucky Supermarket, they have a promotion right now where you can buy six $50 Doordash gift cards and you’ll get 6000 rewards points, which is good for $66 of store credit (and which can be applied to buy more gift cards). Buy with an Amex Gold card and you’ll also get 1200 Membership Rewards points.

How can AT1 bonds be zero'd when they're more senior than equity which is getting paid 2bn, you ask?

Because bondholders agreed they could be.

Here's the section in the $CS 9.75% AT1 prospectus (don't worry if you weren't aware, half the holders prob haven't read this either): pic.twitter.com/Q5FbnOMRM4

Eyes on Tuesday for (again) excessive rainfall with localized flooding issues per @NWSWPC A rapidly developing surface low off the NorCal coast will also bring another round of gusty wind to the region as well. Best to use the relatively quiet weather through Sunday to prepare… pic.twitter.com/al2GNcJCEb

On March 9, Stanford Law students heckled and shouted down a 5th Circuit Judge who was giving a talk hosted by the school’s student chapter of the Federalist Society. Among the grievances of the heavily progressive student body was that the judge had refused to use, in a 2020 opinion, the preferred pronouns of a transgender person who had been convicted of several offenses related to child pornography. (“In conjunction with his appeal, Varner also moves that he be addressed with female pronouns. We will deny that motion.”)

The judge was reportedly unable to complete his prepared remarks, and during question time was subjected to invective, such as the question, “I fuck men, I can find the prostate. Why can’t you find the clit?”

Apparently, when one of the school’s diversity deans arrived to “restore order,” she ended up criticizing the judge, while other administrators failed to tell protesting students to allow the judge to speak without being interrupted.

Student members of the Federalist Society were further subjected to a name and shame campaign, and allegedly “encircled” and abused at the event after federal marshals escorted the judge away.

The judge later remarked, “Don’t feel sorry for me. I’m a life-tenured federal judge. What outrages me is that these kids are being treated like dog shit by fellow students and administrators.”

On March 11, the Dean of the law school, Jenny Martinez, and the University President, Marc Tessier-Lavigne, sent a written apology to the judge:

We are very clear with our students that, given our commitment to free expression, if there are speakers they disagree with, they are welcome to exercise their right to protest but not to disrupt the proceedings. Our disruption policy states that students are not allowed to “prevent the effective carrying out” of a “public event” whether by heckling or other forms of interruption.

In addition, staff members who should have enforced university policies failed to do so, and instead intervened in inappropriate ways that are not aligned with the university’s commitment to free speech.

Dean Martinez followed that up with an email to alumni clarifying the law school’s stance on free speech.

In response to the apology, “hundreds of student protestors wearing masks and all-black clothing lined the hallways outside Stanford Law School Dean Jenny Martinez’s classroom” where she was teaching a con law class. She “arrived to find her whiteboard covered in fliers ridiculing Duncan and defending those who disrupted his speech. The fliers echoed the opinion of student activists and some administrators who claimed hecklers derailing Duncan’s talk was a form of free speech.”

“They gave us weird looks if we didn’t wear black” and join the crowd, first-year law student Luke Schumacher said. “It didn’t feel like the inclusive, belonging atmosphere that the DEI office claims to be creating.”

As a law school alumnus, I found this behavior incredibly embarrassing.

You only have to flip the roles to highlight how ridiculous it is. What if it were a left-leaning circuit judge being yelled at and insulted by a motivated group of right-leaning students? Would the same progressive students who yelled down Judge Duncan support the right’s right to do so then? I doubt it.

I am not familiar with the judge’s jurisprudence, but to be clear, with respect to the viewpoints of his that were reported by the media, I do not agree with them. But that should not matter here.

I can’t think of any other country which has a more expansive right to free speech than the U.S., and it is a fundamental enough right that it is enshrined in the constitution. However, if you seek to wield that right, you wield a double-edged sword. The same right that allows anyone to speak out on political topics without fear of government prosecution, allows other people to picket (at a distance) the funerals of gay murder victims with hate speech. But that is kind of the point. As a result, censorship is something that runs contrary to free speech values, and not letting someone talk by shouting over them en masse is a form of censorship. And, at some point, that kind of disruption can cross the line into unlawful speech—harassment, threats, slander, and the like.

Stanford is a private university and is not legally required to uphold free speech values. However, these values share much in common with the notion of academic freedom, and so it is unsurprising when Dean Martinez writes, “Freedom of speech is a bedrock principle for our community at SLS, the university, and our democratic society. … The way the event with Judge Duncan unfolded was not aligned with our institutional commitment to freedom of speech.”

It’s not clear in the reporting whether the protesters were law school students, or students from other parts of the university (events like these are normally open to all to attend). If they are law school students, what are they going to do when they become lawyers and get in front of a judge they disagree vehemently with, but still need to present a case to?

(Sidenote: Interestingly, unlike the U.S., a few countries like England and Australia, practice the “cab-rank rule” which obliges barristers to accept work from any client as long as they are competent enough to handle it, and regardless of any personal distaste the barrister may have for their client’s reputation, character, etc. “Without the cab-rank rule, an unpopular person might not get legal representation; barristers who acted for them might be criticized for doing so.” So in these countries, you not only need to have the ability to present a case respectfully in front of a judge you may personally hate, but you may also need to do it on behalf of a client you find repugnant. Not easy but, in my opinion, an important part of the justice system.)

Further Observations

Last week’s newsletter about SVB produced the highest number of views out of all my past newsletters. The drama continued this week, with regional banks under pressure. One of the most notable among these banks is First Republic, a San Francisco-based bank that serves a lot of high net worth individuals. First Republic has been experiencing an outflow of deposits which has led to efforts to shore up its balance sheet. In addition to obtaining a $70 billion credit line, a consortium of large banks deposited $30 billion on Thursday. First Republic was reportedly also looking for an acquiror. However, those efforts failed to calm the markets, and the stock closed down for the week, reflecting skepticism that First Republic will be able to weather the storm without going into receivership.

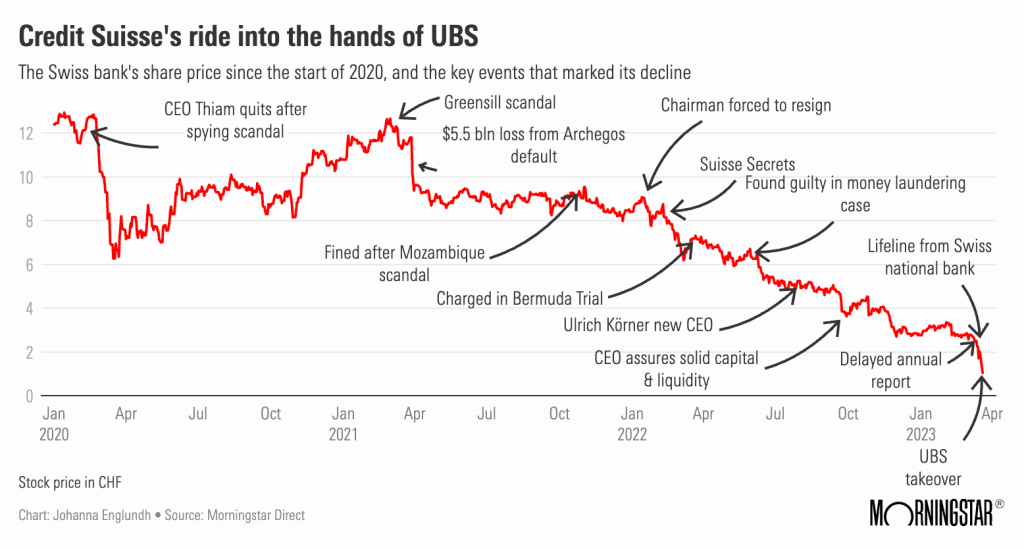

On the other side of the Atlantic, UBS has agreed to buy Credit Suisse for about $3.2 billion in an all stock deal which is expected to close by the end of this year. That’s 0.50 Swiss francs per share, which is about a quarter of CS’ stock price at market close on Friday.

Everything Everywhere All at Once won seven Oscars last Sunday. Unusually, EEAAO took out most of the top shelf awards, including Best Picture, Best Director, and three acting awards, despite being a sci-fi flick. Also unusual was that two Asians from the movie landed two of the acting awards: Michelle Yeoh won Best Actress in a Leading Role, and Ke Huy Quan won Best Actor in a Supporting Role. (Jamie Lee Curtis landed the award for Best Actress in a Supporting Role.) Yeoh is the first Asian winner of her award in Oscars history. Harrison Ford presented the awards, which was a nice touch seeing that Ke Huy Quan last appeared on screen with him in Temple of Doom as Short Round. EEAAO is an absurdist film that I found difficult to follow at times, but it’s quite a spectacle with some memorable scenes, including one featuring butt plugs which people are doing their best to sit on.

Strong winds caused another power outage at our home on Tuesday. It lasted 12 hours for us, but 48 hours for our kids’ preschool. Due to the recent rains saturating the ground, a lot of large trees were uprooted, leading to widespread blackouts throughout the Bay Area. We had to spend a night at a hotel again.

In other news, Tesla has finally started selling its Powerwall on a standalone basis again. Due to supply constraints over the last couple of years, Tesla would only sell Powerwalls bundled with solar panels. The recent blackouts have pushed us towards buying a pair.

Never Split the Difference (Chris Voss) A very interesting book written by a former hostage negotiator for the FBI. It highlights the shortcomings of a more traditional “principled” approach to negotiation, where rationality rules the day, and focuses more on the emotional and human aspects of negotiation. Voss asserts that compromising (”splitting the difference”) is a cheap way out that often leads to sub-optimal results for both parties. Sometimes there’s a way to get all of what you want, even when it appears you have little or no leverage, and without blowing up the relationship.

Hotels

Residence Inn by Marriott San Mateo – San Francisco Airport (San Mateo) Unfortunately, the nearer (and nicer) Residence Inn we stayed at during the last power outage was all booked out. This hotel is older, but still pretty well equipped and pretty good to work from. We got upgraded to a two bedroom, two bathroom suite split over two levels.

Charts, Images & Videos

On Twitter

Danger! Workers are doing too well! Call the Fed to shut that down! A conversation with former Treasury Secretary Larry Summers. Watch the full interview in our latest episode, now streaming on @appletvplus. pic.twitter.com/B6GtO0QLnw

— The Problem With Jon Stewart (@TheProblem) March 17, 2023

You guys know what happened to the stock market the last two times this happened? pic.twitter.com/j0GvICdBB6

1/10 The USG response has likely stemmed contagion. However, $SIVB saga has effectively forced the mkt to price the entire Fed Funds rate into the funding cost of the regional banking system. An acceleration in lending contraction is here.

Silicon Valley Bank is, relatively speaking, just down the road from me. As one the top 20 largest banks in the U.S., it is the banker to half of the startup industry but, fortuitously, not to my employer.

At the start of this week, SVB held about $170 billion of deposits from its customers. On Thursday, it fell victim to a bank run. SVB’s customers, within the space of about 24 hours, withdrew $40 billion—a quarter of its deposit book. This is a tremendous amount, and SVB did not have enough cash on hand. In fact, at the end of the day, it had a cash shortfall of almost $1 billion dollars. When a company is unable to pay its debts as and when they fall due (and on Thursday, $40 billion suddenly fell due), the company is considered insolvent and cannot continue business as usual.

On Friday, SVB was placed into receivership. A federal government agency called the Federal Deposit Insurance Corporation (FDIC), took over management of SVB and immediately closed it for business. Anyone still with money in SVB was now unable to get it out. “Anyone” turns out to be mostly startups, who are now facing an uncertain and very stressful few days.

But how did we end up here? Why did customers suddenly want to pull out $40 billion? And if took in $160 billion in deposits, why did they have not enough cash to pay $40 billion back?

What happened?

We don’t normally think about things in this way, but a deposit in a regular bank account is basically a loan to the bank that you can ask the bank to repay at any time (which essentially happens when you go to an ATM and withdraw cash, or ask Venmo to send money from your bank account to a friend). In exchange for lending money to the bank, they pay you interest (normally). Banks use your money to make money. Typically, this is done by lending those deposits to other people, at higher interest rates. So, for example, you might lend the bank $100,000 and they pay you 1% interest, but then someone else might borrow that $100,000 from the bank to buy a house (i.e. a mortgage loan) and pay the bank 3% interest. They pocket the 2% difference.

But the loans that banks make aren’t “on demand”. If you have a 30 year mortgage, you only need to repay a certain amount, plus interest, each month. The bank normally can’t force you to pay more than that. On the other hand, the money you lend to the bank in a regular savings account is “on demand”. This is sometimes referred to as “borrow short and lend long” and is just how banks work.

So, given that timing mismatch, how can the bank lend any money out? After all, it’s no good if you go to the bank one day and want your $100,000 back, only to be told “sorry, we lent your money to someone else and we have to wait 30 years before we get it all back”.

Enter “fractional reserve banking”. In reality, people rarely ask for all their money back at once, and never does everyone ask for all their money back at once, so banks only need to hold back a fraction of their deposits as cash, and can lend the rest of it out (or invest it in other things that are expected to produce a positive return). The fraction that banks need to hold in reserve is fittingly called the reserve requirement, and is set by banking regulations.

There are situations in which unusually high amounts of withdrawals may exhaust a bank’s reserves, but there are usually also facilities available under which banks can borrow money (typically from other banks) on a short-term basis to fill any holes while they scramble to convert their other assets (loans and investments) back to cash.

SVB was in a slightly different situation, but the basic principles are the same. The main difference is that their client base is heavily composed of tech startups. Most tech startups are not profitable or cash flow positive, so they finance their operations by raising equity financing (giving up a piece of the company in exchange for money), rather than debt financing (paying interest in exchange for money). Missing an interest payment on a loan can be deleterious, so when you’re not reliably making money as a startup, debt can be dangerous and is usually avoided. As a result, SVB didn’t have a lot of avenues for lending out the money it had received from its customers to other customers, so it needed to find another place to invest that money to earn a return.

For this, SVB invested a lot in debt in the form of U.S. treasury bonds and mortgage backed securities. When you buy a U.S. treasury bond, you are lending the U.S. government money, and they pay you interest. Treasuries are considered “risk free” in the sense that the U.S. government will always be able to pay you back. They can do this because they can just print money, if they need to. (Let’s leave to one side for now the game of chicken that politicians play every few years with the debt limit.) So from a creditworthiness perspective, treasuries are a very conservative investment vehicle. They are also a very liquid asset, which means there is a deep and active market that lets you buy and sell a lot of bonds quickly.

Because the short-term interest rates have been near zero for so long, SVB decided to invest in $90 billion worth of longer-term bonds that returned a little less than 2% of interest per year, and the full amount of principal after several years.

During the pandemic years, investment in tech startups blossomed, with equity financing pouring into companies at ever increasing valuations. Consequently, because of how concentrated SVB’s client base is in tech startups, their deposits trebled from about $60B at the start of 2020 to almost $200B just a couple years later.

In 2022, after over a decade of near-zero interest rates, rates began rising sharply, to around 5% today. SVB started to find itself having to pay more interest on its deposits, increasing the need for SVB to earn a return on all that money that its customers had lent it. However, most of its money was locked up in those long-term bonds, which was one problem.

The other problem, is that due to increasing rates, the funding environment for startups tightened right up—instead of investing in startups, more people were now investing in treasuries, which were yielding more than they had for over a decade (and remember, treasuries, unlike startup investments, are considered risk free). On the other hand, tech company valuations were getting slashed. This meant that as startups spent their money, no new funding was coming in to replace it. SVB’s deposits started to fall by billions of dollars as startups withdrew money to pay employees and vendors.

SVB needed to start converting some of its investments back to cash so that it could pay those customer withdrawals. Here’s where the problem started.

Most of SVB’s assets were treasuries. If those treasuries are held to maturity, SVB gets all its money back. But if it needs the money now, SVB needs to sell those treasuries now. Unfortunately, if SVB paid $100 for a treasury bond that only pays $2 in interest a year, no one today is going to buy that bond for $100 because the U.S. government is currently issuing bonds that pay $5 in interest. So if SVB sells those bonds, they are going to have to sell them for something less than $100.

This was a problem for SVB, because let’s say it sold some bonds for 95% of what they bought them for. Accounting rules require SVB to consider that its entire bond portfolio is now only worth 95% of its original value. For a $90 billion portfolio, that’s a $4.5 billion decrease. In reality, it’s reported that the bond portfolio had actually lost $15 billion in value. So if they sold some of those bonds, they would have a massive $15 billion hole in their assets that they’d have to plug somehow (remember, that’s $15 billion they no longer have to cover the deposits they’ve taken in). So those bonds were effectively untouchable in the short term.

Instead, SVB sold substantially all of its other investments for cash—$21 billion worth—it also tapped out some other lines of credit it had. As a forced seller, it incurred a $1.8 billion loss on the sale because those investments had declined in value. To plug that hole, SVB tried to do what all of its startup clients do—raise $1.75 billion equity financing. In the press release for the equity raise, the $1.8 billion dollar loss is mentioned in the last paragraph, almost as an afterthought.

People noticed, and this news spooked people. People started to wonder why SVB decided to liquidate $21 billion at a significant loss, and rumors started to fly about whether SVB was in trouble.

Bank Run

Silicon Valley is a pretty interconnected community and news spreads fast. For example, my CEO was plugged into his CEO and VC network and hearing what was going down. Our head of finance was talking to other heads of finance at peer companies. I was reading buzz from a mailing list with hundreds of head of legal on it. Word started circulating that companies were getting their money out of SVB, just in case. It became an echo chamber.

The other thing about having tech startups as clients is that they are tech experts, not finance experts. A large number of tech startups are run by talented under-35 founders who have not experienced a financial crisis in their professional lives, nor are they finance experts. As a result, they logically turned to their VCs for advice on what to do when the rumors started. After all, VCs are “the money guys” and they should know much more about financial management since that’s the industry they effectively operate in. So when one VC says “get your money out,” that causes a whole bunch of their portfolio companies to do just that.

Having seen how fast things unravelled in 2008 (“Bear Stearns is fine!”), my initial reaction to hearing the news was: Get your money out of SVB right fuckingNOW… if you can. As in, drop whatever you’re doing and get those wire instructions in. If it’s nothing, you can always move the money back.

If you didn’t have a second bank account, or you had a loan with SVB that contractually required you to keep your cash with them, things got a bit trickier, and you then had to make calls like whether to move the cash into a founder’s personal bank account, or ignore your loan covenants, and then worry about any legal ramifications afterwards.

The next morning, and $40 billion in withdrawal requests later, SVB was dead. The FDIC announced that SVB was both insolvent and failing its regulatory liquidity requirements.

There has been some blowback against some VCs for fanning the flames of a bank run that might have been avoidable, but I don’t think VCs are to blame here. As a company, you have to look out for your own employees and business and, in this case, taking your money out if you could was the right call. If it’s a false alarm, there’s little downside. But if it’s real, then you don’t want to be stuck in a tough place… especially if it was avoidable. The herd mentality is a powerful driver of financial markets and you want to at least be part of the stampede—not be crushed by it.

What now?

Through the FDIC, the U.S. government provides deposit insurance at all FDIC-insured banks. If a bank collapses, the FDIC will ensure that depositors will be able to get at least $250,000 of their funds back. (This limit used to be $100,000 but was raised after 2008 Great Financial Crisis.) This is very helpful for the average person, who is likely to have less than $250,000 cash lying around in a bank account. It is not so helpful for a company, that is likely to have much more than that. Apparently, about 96% of SVB depositors were not fully covered by FDIC insurance, compared to about 38% at Bank of America.

This insurance kicks in very quickly. On Friday, the FDIC created a new bank called the Deposit Insurance National Bank of Santa Clara (DINB). The insured portion of all SVB bank accounts was then transferred to the new bank, and depositors will have access to those new bank accounts on Monday. The uninsured portion of those bank accounts (anything over $250K per depositor) was then effectively frozen, with the FDIC issuing a “receivership certificate” to each depositor that represents an unsecured claim on the remaining assets of SVB up to the amount of the uninsured funds.

Next, the FDIC’s job will be to sell off SVB in a way that maximizes the money they receive. That money is then distributed to a list of people, starting with secured creditors, then depositors, then other unsecured creditors, then subordinated debt holders, then anything remaining goes to SVB’s stockholders.

As the FDIC sells off SVB, it will issue a dividend to receivership certificate holders. It’s rumored that the FDIC has been hard at work flogging off tens of billions of dollars’ worth of SVB’s assets and will issue an “advance dividend” of about 50% of the value of a certificate sometime in the next week.

The best outcome now is for another bank with a strong enough balance sheet to buy SVB and assume all the deposits in one fell swoop, which will allow accounts to be unfrozen. I think that is a likely outcome. If that doesn’t happen, then SVB will be sold off in pieces, and uninsured depositors will get their money back over time. I think that depositors will get most, if not all, of their money back, but it will take months, or even years.

In the meantime, the timing uncertainty and inability to access funds is incredibly stressful to affected startups. Payroll is due next week. Failure to pay wages is one of the things that can “pierce the corporate veil”, meaning that liability for that failure spills beyond the company, and may impact officers, directors and stockholders personally. However, one would think that if employees get paid a few days late, they’re going to be understanding and not litigious.

This weekend, startups are trying to find sources of immediate-term funding, ranging from loans from VCs, bridge loans, credit cards, and selling their receivership claims at a discount to opportunistic investors.

And teams of bankers, lawyers, and bureaucrats are spending a sleepless weekend trying to figure out what to do with SVB before the markets open on Monday.

I think the majority of SVB startups will be fine at the end of the day. There may be a severe liquidity issue for startups with short runways (e.g. if you had a 12 month runway and only get 50% of your funds back next week, you now have a 6 month runway and no idea when the remainder of the money will come back, and you’re now thinking about whether you need to lay off people to conserve cash).

[UPDATE: It’s over; startups can feel relief. 30 minutes before this post was scheduled to go out: ‘The Federal Reserve, Treasury and Federal Deposit Insurance Corporation announced in a joint statement that “depositors will have access to all of their money starting Monday, March 13. No losses associated with the resolution of Silicon Valley Bank will be borne by the taxpayer.” The agencies also said that they would enact a “similar systemic risk exception for Signature Bank,” which the government disclosed was closed on Sunday by its state chartering authority.’ (per the New York Times) “Separately, the Federal Reserve announced that it was creating a new lending facility for the nation’s banks, designed to buttress them against financial risks caused by Friday’s collapse of SVB.” (per the Washington Post).]

Bail outs?

Several prominent VCs and investors have been screaming for the federal government to come in and backstop deposits in full—not just $250K. In other words, the government should effectively insure everything, and then get reimbursed as FDIC sells off SVB.

This is not a bailout of SVB. SVB is no more—its board and executive team will find themselves looking for new employment (if not already), and the equity holders will likely be wiped out.

But it is a bailout of depositors, and that has other people screaming that the U.S. taxpayer should not have to do that either. Let capitalism take its course. (And, as usual, the whole situation has been politicized.)

The issue is more nuanced than that. As I mentioned above, although depositing money at a bank is essentially lending the bank money (and therefore a form of investment), people don’t really see it like that. And you’re not really thinking that the 16th largest bank in the U.S., which has been around for 40 years and is regulated, is a credit risk. The average person on the street certainly isn’t going to be thinking about that. They’re just looking for a place to put money that isn’t under their mattress. During my time in the U.S., I have had personal bank accounts at a lot of different financial institutions (more than half a dozen), and creditworthiness was never something that crossed my mind.

So is it fair or desirable that depositors should suffer—particularly when what we are talking about here are small innovative businesses that employ thousands of people between them?

But then should we just make FDIC insurance unlimited for everyone going forward? If not, why not?

Some suggest that a failure by the government to backstop depositors here will catalyze a chain reaction that leads to catastrophic bank runs at other (small) banks. The argument goes that why would anyone put money in a smaller bank that is at risk of a bank run? People will just move money into the biggest 4 banks in the U.S., which will cause further bank runs, kill small banks, and lead to more concentration and less competition in the banking industry, which is bad for everyone. I’m not very convinced by this argument. I think we are in a specific situation exacerbated by the uniquely concentrated customer base that SVB had (only 3% retail clients!) which produced a high proportion of uninsured deposits.

This was also a liquidity issue, not a situation where SVB plowed billions into FTX stock that is now worthless and they now can’t cover the hole. SVB apparently has enough assets to cover its deposit liabilities—it just needs time to sell them off. People probably aren’t going to lose a lot of money, unlike when your crypto exchange goes belly up.

As for the question why anyone will now deposit in small banks if there’s no backstop—in most banks, the existing backstop covers most depositors. Secondly, why do people bank with smaller banks today? Because their product is positively differentiated in various ways. I’m skeptical that the perception of a potential threat of a bank run happening to a smaller bank is going to outweigh all the other reasons that smaller banks exist in a way that leads to an existential crisis for them. But let’s see what happens when the markets open on Monday.

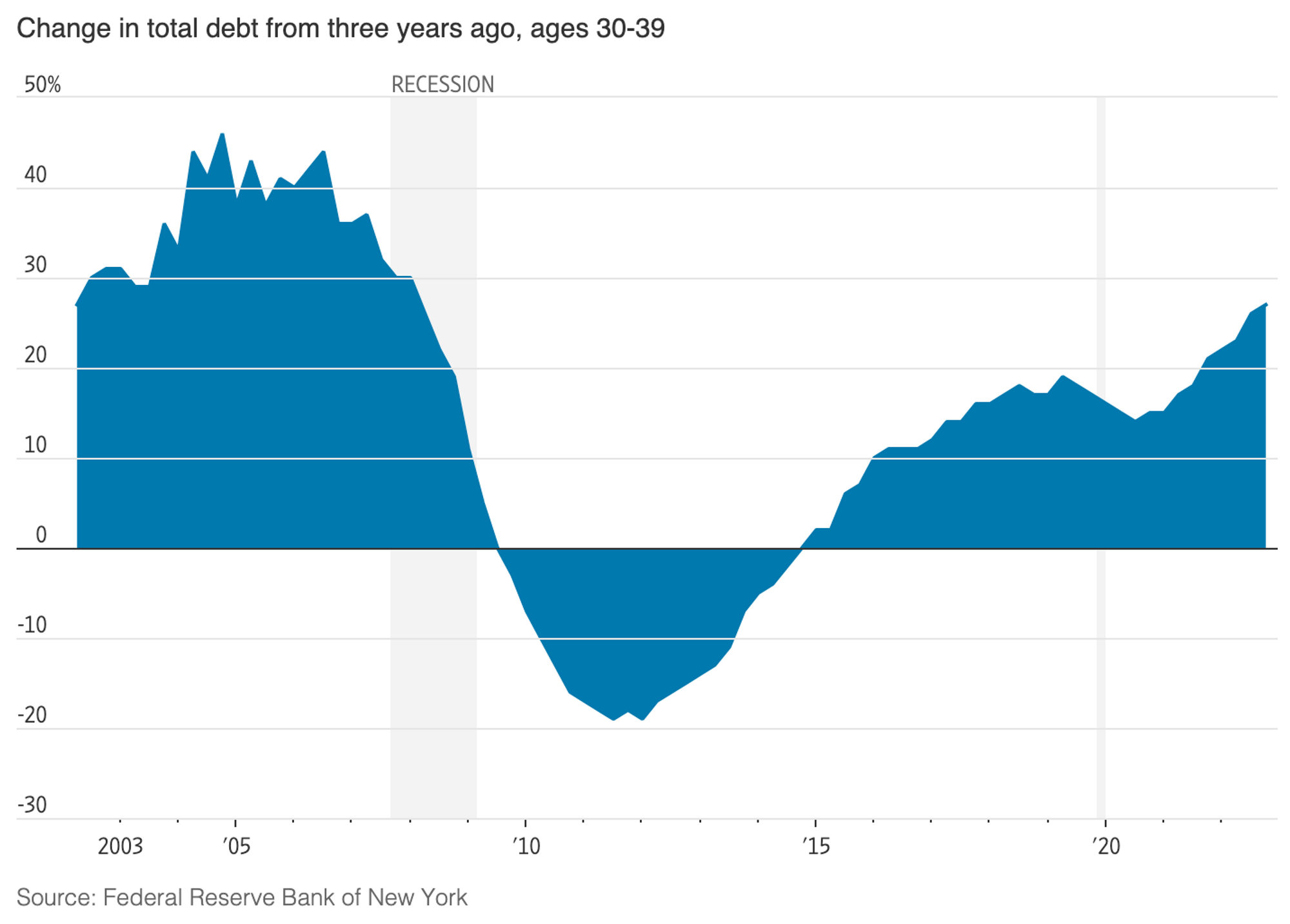

Another thing that is clear to me is that we now have a generation of workers who have been exposed to a financial crisis for the first time. To be sure, it’s mostly localized to tech startups (for now), but for almost 15 years now, money has been cheap and free-flowing and the last 9 months have been a huge shock to the system. It will be intriguing to see how these interesting times shape the psyche of Gen Z and younger millennials, just like how the financial habits of the Silent Generation were shaped for a lifetime after growing up through the Great Depression.

More to come

I still think the worst is yet to come for the economy as a whole. If interest rates are sustained at current levels (and it’s starting to look that way, as employment is still strong and inflation remains elevated), we’ll start to see them bite into the parts of the economy that are the most sensitive to rate rises, and that will cause a domino effect. I’m not sure where that is, but I could see, for example, companies that have maturing loans getting into trouble when they have to refinance at much higher market rates. Or unrealized losses that bondholders being forced to be realized due to liquidity needs.

If you spend much time on AI twitter, you might have seen this tentacle monster hanging around. But what is it, and what does it have to do with ChatGPT?

It's kind of a long story. But it's worth it! It even ends with cake 🍰

The failure of @SVB_Financial could destroy an important long-term driver of the economy as VC-backed companies rely on SVB for loans and holding their operating cash. If private capital can’t provide a solution, a highly dilutive gov’t preferred bailout should be considered.

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank. Absent @jpmorgan@citi or… https://t.co/SqdkFK7Fld

Warren Buffett’s annual shareholder letter was published as part of Berkshire Hathaway’s annual report last week. This year’s was quite brief, but as usual, very accessible and a repeated reminder of the simple themes that have served him well over the decades.

After the growthy period of 2019-2021, Berkshire returned to outperforming the S&P index, returning 4.0% in a year where the market fell 18.1%.

“We are understanding about business mistakes; our tolerance for personal misconduct is zero.”

Berkshire buys businesses and also invests in public companies with the expectation of holding each indefinitely and therefore looks for enduring businesses with trustworthy managers. He notes that private, controlled businesses are almost never available at bargain valuations.

He notes that they make, on average, one “truly good” decision every 5 years, and that the performance of their portfolio of businesses includes “a large group that are marginal” but many that are “very good” and a few that are “truly extraordinary”.

For example, he highlights the performance of a 28-year holding of Coca-Cola. Cost base was $1.3B. As of 2022, it threw of $704M in cash dividends (53% annual yield on the original investment!) with a market value of $25B (19x capital gain).Put another way, if my parents had invested $100k in Coke when I was in primary school, that investment would today be almost $2M and generating $53k in dividends. Makes me think about what I should do for my kids to leverage the power of compounding. They are each currently, as Morgan Housel puts it, “time billionaires”.

Last year, Berkshire acquired another property-casualty insurer, growing its insurance float from $147B to $164M (the premiums it holds).

Berkshire holds a “boatload of cash and U.S. Treasury bills” and avoids behavior that could result in uncomfortable cash needs at inconvenient times, including financial panics and unprecedented insurance losses. Seems like a good personal approach too.

He rails against the politicization of stock buybacks. As a pure matter of mathematics, stock buybacks, when performed at a good (undervalued) price, are beneficial to all remaining shareholders.

His formula: retaining earnings in its businesses (Berkshire doesn’t pay dividends) + compounding + avoiding major mistakes + what he calls the American Tailwind: “America would have done fine withour Berkshire. The reverse is not true.”

Berkshire’s annual corporate tax bill of $31B is 0.1% of the entire American tax base.

He shares a bullet point list of some things Charlie Munger said on a podcast, including the value of being a patient, long-term investor, the dangers of leverage in wealth destruction, that you “don’t need to own a lot of things to get rich”, and that investing requires adapting as the world changes.

In reference to Charlie Munger: “Find a very smart high-grade partner — preferably slightly older than you — and then listen very carefully to what he says.”

Phones at Work

When I was younger, I generally disliked talking on the phone (there was a measure of anxiety attached to it), so the advent of SMS, emails, and IMs felt like a blessing to me, and more so as the younger generations pushed adoption of that socially, and then in the workplace. However, especially in tech workplaces, I now find myself missing phone calls.

To contact someone now, people typically reach out via Slack and then wait. Or schedule some time on their calendar and then wait. Or if it’s really urgent, they’ll send a text and then wait. It’s less intrusive, but also there’s no way to guarantee a quick answer for small things — even if the person is completely available, they just might not see your message for a while. And for a lot of these calls you simply don’t need video. You just need to get some shit done.

When I was a junior lawyer at a firm, we had these Cisco IP phones on our desk. People would just dial each other up by punching in 4 digit extensions. It was spontaneous, marvelously tactile, and it wasn’t a big deal. If the other person was unavailable (in a meeting, on another call, or just under the gun getting something out), they would ignore the call or send it to voicemail. (And if it was super urgent and you weren’t answering, they would physically show up at your door.) No one really worried about interrupting anyone. Clients would call out of the blue as well.

For a period I had an office next door to my supervising partner (I still remember his 4-digit extension, 15 years on), and he would still call me despite the physical proximity. I was thankful that he didn’t scream through the wall, even though that would have been marginally quicker.

These calls were a great way to deal with things in a minute that can now take quite a lot of minutes and relative effort to resolve over chat. Also, it’s a great way to ask a bunch of questions in a way that feels natural but, when done over a textual medium, can feel interrogational and even aggressive.

No one does this anymore, and I think you lose a valuable communication method and tool.

Further Observations

This week I learned that the U.S. Supreme Court opens each term with the pronouncement “Oyez, oyez, oyez!” Oyez is an Anglo-Norman word that means “Hear Ye!” It’s kind of weird that it took me so long to learn that given that I work in law and also started a blog called Hear Ye! over 20 years ago.

A 15-lawyer Canadian litigation law firm tried the 4-day work week for 2 years and published its results (Wednesday was their off day). They are pragmatic and interesting:

“Sometimes you’d have to work 5, 6, or 7 days a week and that is OK; that’s just life.” In other words, at a normal law firm you sometimes have to work weekends. In this case, the weekend is 3 days long, and you may have to work weekends. Particularly since clients expect availability and the courts have their own schedules. “In my interviews with our lawyers, they said they have had to work at least 1 hour or more on over 50% of Wednesdays.”

“You can attract the wrong crowd by advertising 4-day work weeks and need to get your message right and clear.” They put in a 3 month probationary period that requires new hires to work 5 days in the office until they get an idea of their work ethic.

“We have way, way less turnover.” This makes sense. And this suggests people chuck sickies quite often: “Our sick day requests have been reduced by over 80%.”

They still managed to grow revenue over that period (more than 2x over 2 years).

Drive to Survive (Season 5) “It’s not a documentary. It’s closer to Top Gun than a documentary.” —Toto Wolff. Great way to whet the appetite for the new F1 season, which started this week!

There's an easy way to measure Google's moral temperature at any given time: how closely the ads resemble the search results. pic.twitter.com/QZ15aOa0Ak