Please note: The posts on this page are at least 3 years old. Links may be broken, information may be out of date, and the views expressed in the posts may no longer be held.

It’s a long holiday weekend, so a light update for this week. Happy Thanksgiving!

We went to CostCo on Friday and they were selling full Thanksgiving meals marked down from $40 to $15. I’m guessing they thought everyone was going to be all turkeyed out, but we’re never ones to turn down a great deal!

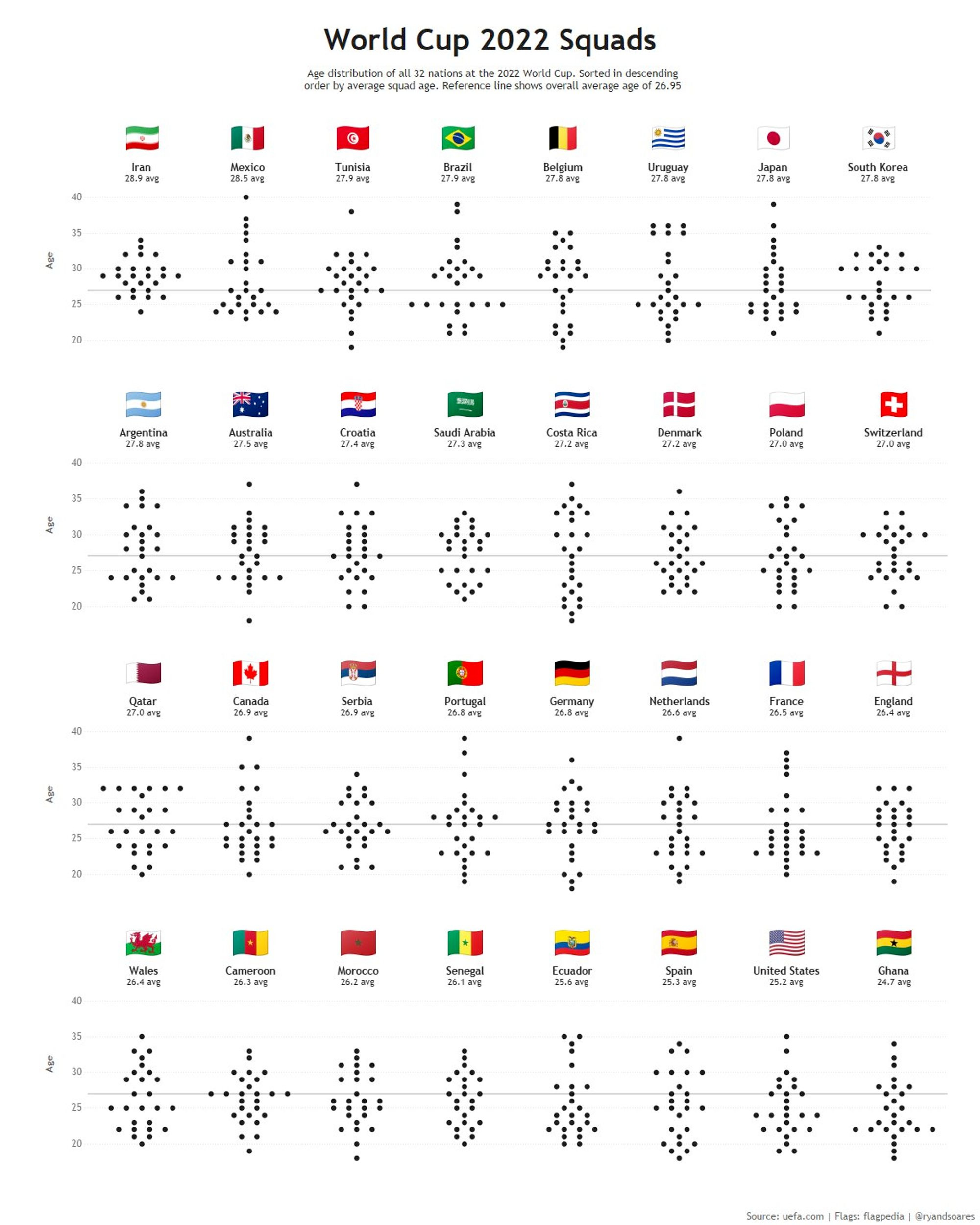

World Cup updates after 28 games:

Lots of upsets! France looks pretty solid.

Fantasy League: 5th out of 14 after the first week.

Head-to-Head Betting: Started off with a bad run but clawed most of it back after calling 5 games in a row.

Andor (Season 1) Almost universally acclaimed, and for good reason. I found the Narkina 5 storyline particularly enthralling.

Hotels

InterContinental San Francisco (San Francisco, CA) We spent part of the weekend up in the city and used a free IHG night here. The hotel feels aged and nothing to write home about. The showers were terrible, with the water constantly fluctuating between hot and cold.

The 2022 World Cup kicked off today in controversy-riddenQatar. The time zone is poor for where we are, with most matches occurring in the early morning.

I participate in two longstanding World Cup traditions. The first is a fantasy league which is running for the sixth time (which means the first was held 20 years ago when I was an undergrad!). Nothing is on the line except glory. We got a trophy made and every 4 years we engrave the winner’s name on it. I normally tend to fare pretty well but I’ve never won it and the victors always like to channel Ricky Bobby: “If you ain’t first, you’re last!”

The second is a 1 on 1 betting match where a friend and I bet on every single match against each other. After the group stage, we progressively increase the wager as it moves through the knockout stage, and add bonuses for penalty shootout outcomes. We alternate selecting the winner of each match, using Asian handicaps from this site to keep it fair. It’s all tracked in a Google Sheet and we added columns for gloating and sledging each other after each match. We sometimes do this for the Euro championships too, and the results are normally quite close… although I typically find myself on the negative side of the ledger. We now both live on opposite sides of the planet, so settling the debt sometimes takes time and creativity. (For 2018, my friend asked me to spend his winnings on Powerball tickets, which returned less than the cost of the tickets. I still owe him for my losses in the 2021 Euro Cup.)

On the home front, my family represents 3 different nationalities, each of which is participating this year: Australia, Denmark and the USA. For the second World Cup running, Australia, Denmark and France find themselves in the same group. Alas, Australia is not expected to survive the group stages.

0/ The story of Alameda and FTX can best be summarized by @SBF_FTX's philosophy of betting big.

Every major decision they have made is related to acquiring more leverage – via deceptive fundraises, financial engineering, and ultimately, outright fraud, as we will see below.

Michael Lewis' next book is about Sam Bankman-Fried. Email from CAA confirms he has been embedded with him for last 6 months; note below was first sent to potential buyers for filmed rights. Scoop @TheAnklerhttps://t.co/VcFEmeCAIMpic.twitter.com/ZrioMu7qbb

This week was one of those “weeks where decades happen”. It’s been endlessly fascinating and entertaining. Let’s get into it.

FTX!

You can read about what happened in all the articles linked below, but here are a few things that struck me about the situation.

FTX hit a $32 billion valuation within 3 years and dealt with tens of billions of dollars. It all vaporized in the space of a little more than 3 days. Typically when an organization gets to that scale, the founders bring on seasoned execs. That didn’t happen at FTX. (This is in part a failure of FTX’s investors, who felt so much FOMO that they were satisfied with whatever surface-level diligence they performed and willing to overlook the fact they had no board seats or other protective rights that VCs typically have.) Not only did it remain an underweight organization (apparently with only about 400 people, compared to Binance with almost 20x that), but if you look at the key players, including of their sister trading shop, Aladema Research, they are almost all inexperienced. Reports are that a bunch of them lived out of a shared $30+ million penthouse in the Bahamas and dated each other.

Caroline Ellison was the CEO of Alameda and, at 28 years old, mostly managed SBF’s money and reportedly dated him “at times”. She graduated from Stanford with a math degree in 2016 and had only one job prior to Alameda — 19 months at storied firm Jane Street as a quant trader. In a now infamous video, she mentions that “being comfortable with risk” in the job is “very important” and that they “tend not to have things like stop losses”. Risk management was clearly not her forte and she seemed to confuse being comfortable with risk with being reckless with risk.

Constance Wang was COO of FTX. She graduated from NUS in 2016 with 2:1 honors and took an entry-level job at Credit Suisse working as an analyst doing AML/KYC checks and risk controls. She was there for barely 2 years, jumped over to another crypto exchange (Huobi) for 8 months and then took the COO role at FTX. This site mentions that “Wang clearly wasn’t responsible for the misfortune that’s befallen FTX,” but she took the title and in any other firm managing that amount of money in a position with that title, you pretty much are responsible in some capacity.

Gary Wang (Zixiao Wang) co-founded FTX but appeared to avoid the limelight, unlike SBF. He attended MIT (like SBF) and apparently met SBF at a math camp in Canada.

Dan Friedberg was Chief Regulatory Officer at FTX. Apparently, Friedberg was embroiled in an online poker cheating scandal and cover up in the past — a period of time that reportedly appeared as a big gap in his now-deleted LinkedIn profile. Friedberg was either a partner or counsel at Fenwick & West running their blockchain practice from Seattle. He took the job after the poker scandal, so one wonders what kind of due diligence both Fenwick and FTX did on a pretty darn senior legal hire (and if they knew about it, why didn’t they care?). It appears that Friedberg joined as General Counsel but then transitioned over into the regulatory role after Can Sun joined.

Can Sun joined as General Counsel in mid-2021. He was a colleague of Friedberg in Seattle and co-chaired Fenwick’s blockchain practice with Friedberg. Sun certainly has pedigree (Yale Law, PhD from Princeton, a year at David Polk followed by almost 7 years at Fenwick as an associate), but no in-house experience prior to FTX. Sun abruptly resigned (as did most of his legal team, it was reported) a couple days after the news broke.

Sam Bankman-Fried is the son of two tenured Stanford Law professors — Professor Bankman (who teaches tax law at SLS) and Professor Fried (now emerita). According to his LinkedIn profile, he graduated in 2014 from MIT and was at Jane Street for a little over 3 years. He founded FTX after reportedly making a shit-ton exploiting the many crypto arbitrage opportunities that opened up around 2017 via Alameda Research. (Me and a couple friends got in on this action at the end of 2017, but our scale was many orders of magnitude smaller than what SBF achieved.)

I looked at Alameda Research’s site before it was taken down. It had the team’s photos on there and they all looked young.

From these profiles, you can see one main theme emerge: inexperience. There’s also nepotism, but that happens all the time in tech startups, and it’s not necessarily a bad thing as long as the person being hired is a good fit for the job.

Inexperience, though, is far more dangerous — particularly in a field where you’re dealing with other people’s money. This is people’s lives, we’re talking about. The fallout will be felt in the coming weeks and months, but some people have now lost a huge amount of their life’s savings, and suicide risk is real. There are also signs in the news that the reason for the gaping $8 billion hole in FTX’s finances extends beyond manifest incompetence to some sort of criminal malfeasance. At the least, the abuse of client funds in the manner reported in the media would likely be criminal in TradFi.

Which brings me to my thoughts on the crypto space as a whole. I believe there are two types of people: (1) principled “believers” who are genuinely invested in the technology and the promise of building something actually useful with it, and (2) people who see an opportunity to make money. There are a lot more of type 2 than type 1. And there are a lot of people who claim to be type 1 but are really type 2.

Crypto is a modern day gold rush — people see fortunes to be made and flock out to the wild west.

There’s nothing wrong with that, of course. But when you’re there to make money, it doesn’t matter whether it’s crypto or DeFi or TradFi… it’s just finance. The difference is that TradFi is build up on centuries of experience, and the regulatory framework is developed.

There’s a lot about crypto that’s new, but that’s often confused with what’s not, and the crypto world is “rediscovering” learnings that are already well-trodden in TradFi — such as basic risk management and the dangers of leverage. (This reminds me of a time back when Netflix was still mailing out DVDs, I saw a post online asking “Why isn’t there a startup where we can borrow books, like a Netflix for books?” only to receive a disgruntled reply, “Yeah, it’s called a library.”)

The wild west metaphor is apt because crypto is relatively unregulated. That is just fine for the many crypto enthusiasts with libertarian leanings, but in the real world that means people lose their figurative shirts as a result.

This is not to say that TradFi doesn’t have its Big Problems. The GFC in 2008 is clear evidence of that, and the fact that it led to bailouts was a travesty. But TradFi doesn’t see the speed and sheer frequency of damage that the crypto space has inflicted on consumers (and institutions). Pump and dump schemes, market manipulation, and fraud are commonplace. Literally billions of dollars have vanished this year alone due to hacks or coding flaws. Entire crypto exchanges fold. And it’s mostly unchecked — there are few consequences for perpetrators of some of these schemes, and it just attracts more scammers.

One blessing is that crypto is mostly separate from the mainstream economy, so we haven’t really seen much, if any, contagion. And that’s just the thing — it’s never going to be mainstream as long as it’s unregulated or weakly regulated. It’s never going to be a tool that a family uses (or should use) to buy a house, or keep their retirement savings in.

In the same way that communism sounds kind of OK in theory but is very different in practice due to human nature, I feel the same way about unregulated crypto.

There’s a common refrain used by crypto enthusiasts arising from the FTX disaster: “Not your keys, not your coins.” (This refers to how if you don’t have the private keys that signify ownership of cryptocurrency, you don’t actually own it at all. When you buy Bitcoin from an exchange like Coinbase, they are actually coins owned by the exchange (you hope), and they assign ownership of those coins to you on paper. But you have to withdraw the coins out to your own wallet if you actually want to ensure ownership. Better yet, keep them in cold storage.)

There’s a slight edge to that axiom: it’s your own damn fault if you decided to buy crypto through a centralized exchange — you assumed the risk. If you want to ensure that doesn’t happen to you, keep your coins under your own digital mattress. And that’s just it — it’s not practical. If I want to daytrade crypto, I can’t do that easily through my Ledger wallet. It’s just not convenient. I need an exchange. (I know there are decentralized exchanges, but they have their own issues and don’t solve the underlying problem of lack of regulation.)

So, until the various government agencies get with the program and start regulating things in a thoughtful manner, crypto is not going to replace TradFi in any meaningful capacity, and it’s just going to be a place where both really interesting innovation occurs, and where people get their faces ripped off by avarice.

A sidenote on NFTs: IP lawyers I’ve spoken to are confused why NFTs have any value, given there is a valid question about the worth of the intellectual property you actually own. Similar to how DeFi is still finance, NFTs to me are just luxury goods. Value is in the eye of the beholder, and luxury goods are the epitome of when intrinsic value diverges from perceived value. That’s all it is.

A Birkin bag, or the Mona Lisa, is only valuable because enough people think it is. The materials for a Birkin do not cost $30,000 and the bags do not provide utility that is worth $30,000. But a knock-off Birkin is considerably cheaper than a genuine one. NFTs are exactly the same. They are intangible luxury goods. It doesn’t really matter that from a legal perspective, it’s questionable what, exactly, you own. It doesn’t matter that your picture of a bored ape can be copied with a couple clicks of a mouse (I mean, that kind of sums up the whole software industry). All that is irrelevant. NFTs have value because people believe they have value. And, like the tulip bulbs of the 17th century, if the fad passes, that value will evaporate. The question is: will the value endure?

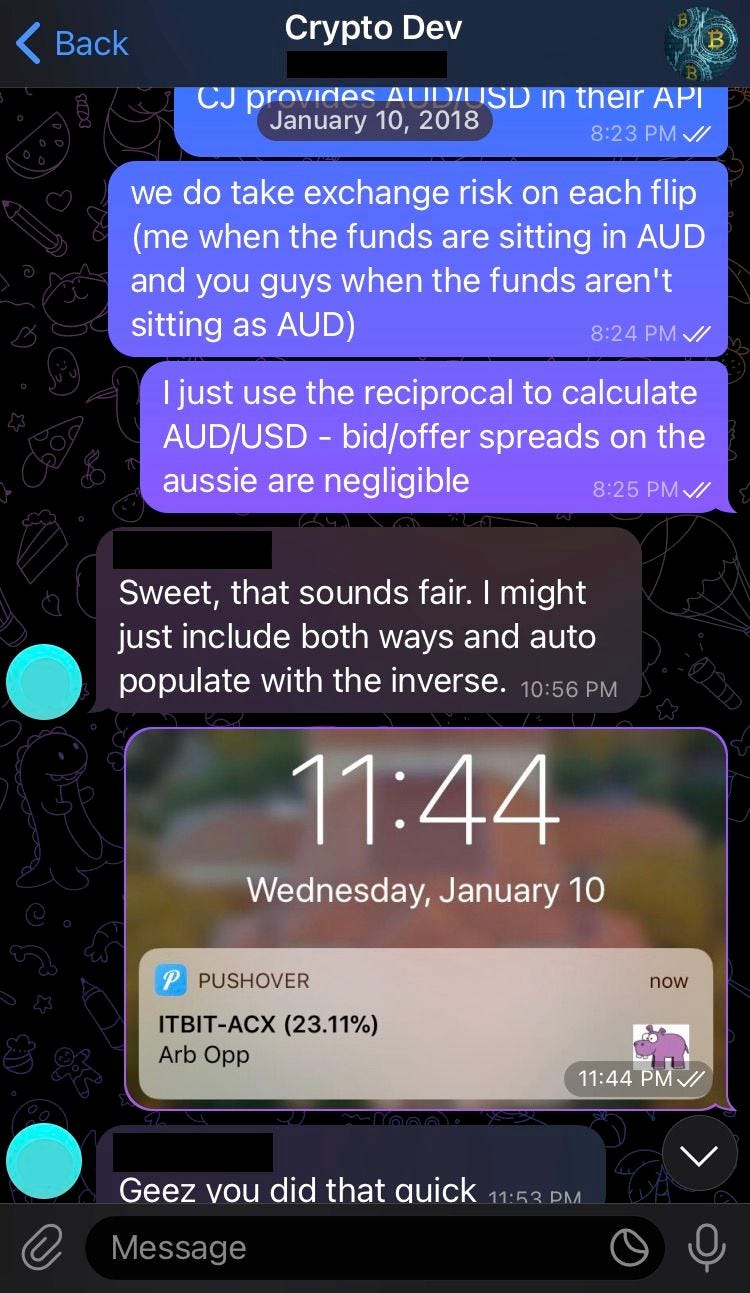

The glory days of inefficient global crypto markets when we could make 23% on a single trade!

Twitter

Damn the torpedoes, full speed ahead!

I feel for what Twitter employees are going through at the moment. The two weeks after the acquisition have been a case of doing everything that good management practices say you shouldn’t do. It sounds like a terrible working environment.

Yet, there is a certain fascination about whether this might actually turn out ok — or even well — in the end. This whole thing is a bit of an experiment. This is a unique situation, and no one’s had the ability, gall or gumption to try what Musk is trying at this speed and scale.

There is a difference between taking a huge but calculated risk and being reckless (see Alameda Research, above), but for the Twitter x Musk combination, this may only become clear in hindsight.

Can you cut 50% of the workforce within 2 weeks, push out features without much apparent thought or planning, send everyone back to the office on no notice, do all the other stuff that’s happened there, and still manage to pull a company out of a spiral? I am not hopeful, but if this is even possible to pull off, I suppose it can only be someone like Musk. CEOs around the world are watching.

Elections. Well, my prediction last week was wrong. With the Dems holding the Senate, I’m pleasantly surprised at the outcome of the mid-term elections. And Trump has been even more unmoored lately and it looks like it’s turning people off.

Meta layoffs. 11K+ people were laid off at Meta this week. The company is still a cash cow, but I think Zuck’s “bet the company” approach on the Metaverse is doomed.

Inflation. On Thursday, the inflation number printed lower than expected. The stock market ripped up and the U.S. dollar fell. However, we’re far from out of the woods.

Lunar eclipse. In the early hours of Tuesday morning, the last full lunar eclipse in 3 years occurred. Unfortunately, it was raining and overcast where I am.

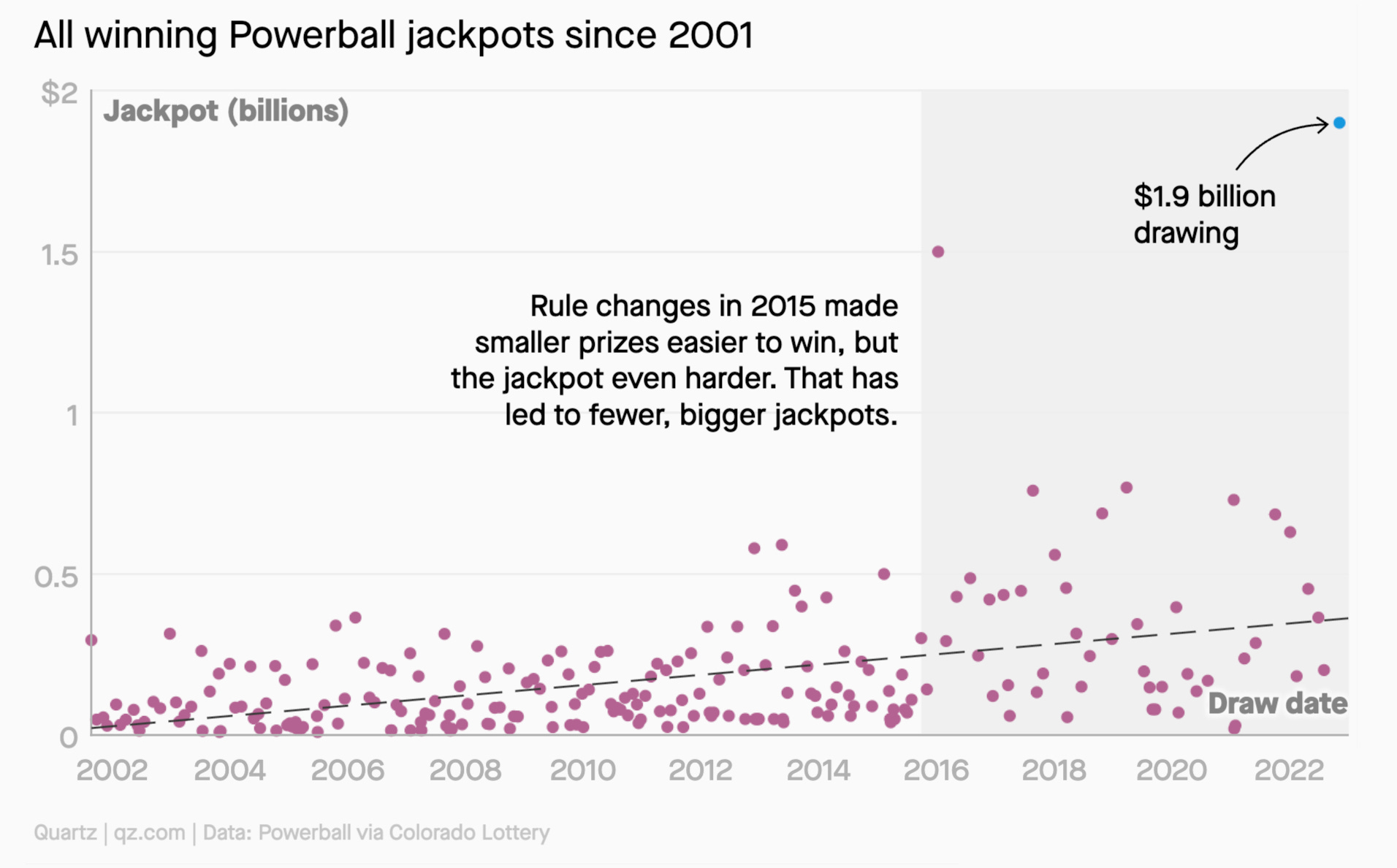

Powerball. A single person won the $2.04 billion Powerball jackpot on Wednesday.

The headline $2.04 billion jackpot is based on taking payouts over 30 years. Paid as a lump sum, the cash prize is $929.1 million, which is based on discounting future cash flows back to present values (you could invest the $929.1 million into treasuries yourself and end up with the same ~$2 billion). This calculation is sensitive to interest rates, which are higher than they’ve been for almost 15 years, allowing Powerball to advertise such a large headline figure.

The prize is taxable, but because the winning ticket was bought in California, no state taxes apply.

Yeah, we bought ourselves 5 tickets. Out of the 30 numbers that we got, only 1 matched a drawn number.

The Powerball jackpot was so big that the display at our local supermarket ran out of numbers

Articles

Pretty much just FTX and Twitter articles this week…

Sam Bankman-Fried Has a Savior Complex—And Maybe You Should Too (Sequoia Capital) Posted on the legendary VC firm’s website (who just lost their $210 million investment in FTX), this article feels completely cringeworthy today. It was taken down from Sequoia’s website a couple days ago, but the internet remembers.

but perhaps we shouldn't have trusted ten kids in their 20s all F'ing each other in a $200M orgy house in the Bahamas with our money on an unregulated exchange

Halloween was on Monday. My wife and I didn’t grow up in America, so Halloween still feels foreign to us. We used to be able to ignore it. (We still could, I guess, but that would be mean to our kids.) It’s my least favorite holiday. For one, it normally falls on a weekday, so it’s not even really a holiday. It’s work and effort.

We went trick-or-treating in the Allied Arts neighborhood of Menlo Park, near where we used to live. It has a good density of houses and throngs of trick-or-treaters which makes for a good atmosphere. It’s also an expensive area so the variety of quality giveaways is typically pretty good. The kids had fun, at least.

Because we were out of the house, we left out a full bowl of candy, which was a mistake. Our security camera showed a group of 5 tweens rocking up early in the evening and emptying the whole thing. At least they didn’t take the bowl, which apparently was a problem for some people in our neighborhood.

Election Day is on Tuesday. I think the Republicans will easily retake the House and Senate, and then we have 2 years of a Congress where even less gets done.

Lots of painful layoffs at tech companies this week. Musk fired half of Twitter on Friday. I actually think Twitter will be fine despite suddenly feeling short-handed. If that turns out to be the case, that suggests that previous management left a lot to be desired. But you still have to feel for the people who find themselves heading into the holiday season unemployed.

The Fed raised interest rates by another 75bps this week, as did the Bank of England. The RBA only raised rates by 25bps, which I think is just crazy. I reckon the Fed will raise by another 50bps in December. Some of our savings now earn more interest than we pay on our mortgage.

Daylight Saving Time ends this Sunday morning. I actually like waking up in near darkness because it makes me feel like I’m waking up earlier than I actually am. (I like the idea of rising early. My body hates the practical reality of it.) Nonetheless, America might be transitioning to permanent daylight savings time at some point, which essentially means that California will become a UTC -7 time zone. The Senate passed a bill in March — the Sunshine Protection Act — that would achieve that… but the House has yet to vote on it.

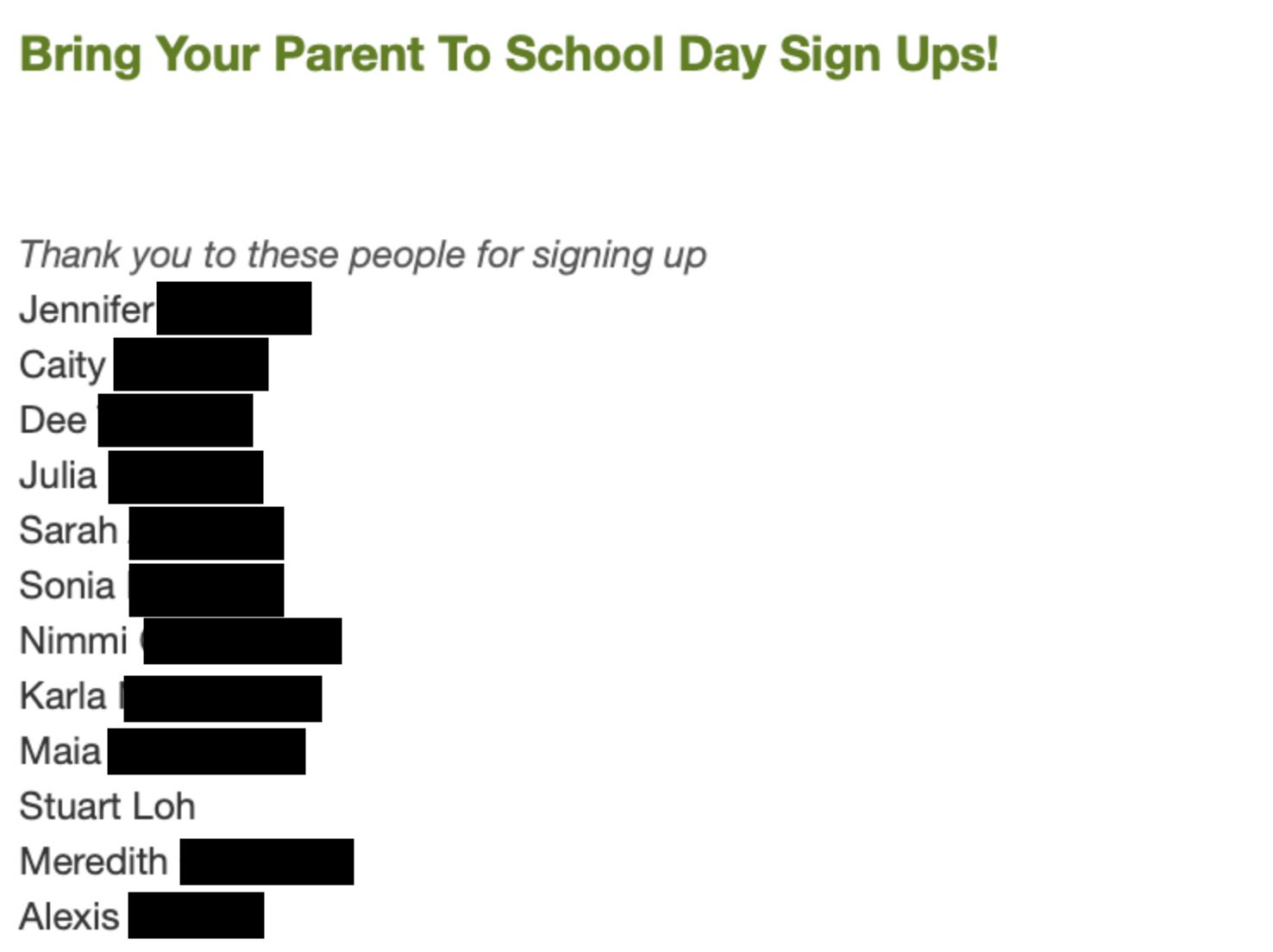

In case there’s any doubt that women do the lion’s share of caring for kids, this is the sign up list for an event at our pre-school (one parent from each family was requested). Most, if not all, of these are working mums.

Biglaw Firm Tells Associates Exactly How Many Times They Need To Check Their Emails Over The Weekend (Above the Law) Slaughter & May’s answer: Once on Friday night, and twice a day during the weekend (except 10pm – 8am), unless you’re working on a matter that demands greater availability. “We’re a bit like a five-star hotel … [clients know] that if you call room service at 2 a.m. for a sundae, you’ll get one” is correct, even though it can be a very exacting (but well-compensated) job. If my employer is paying $800-1000 an hour for an associate, we better be getting Rolls-Royce service. If you had to pay any other person working in the service industry $1000+ an hour, you’re going to expect them to deliver client service with rings on their fingers and bells on their toes. Sadly, this is not always the case.

Amazing what a consumer drone can do in air that thin

On Twitter

I've now been asked multiple times for my take on Elon's offer for Twitter.

So fine, this is what I think about that. I will assume the takeover succeeds, and he takes Twitter private. (I have little knowledge/insight into how actual takeover battles work or play out)